5-2 Review and Reinforcement Reading the Periodic Table

If you want to go on upwardly with loan payments, peculiarly when it comes to a fixed-interest loan, using an amortization tabular array can be incredibly helpful. Not merely tin can a loan amortization tabular array assist you keep up with your monthly payments, but it's also great for agreement your interest costs as the loan balance decreases. Not familiar with how an amortization table works? Don't worry — nosotros'll walk you through how to make, read, and use one.

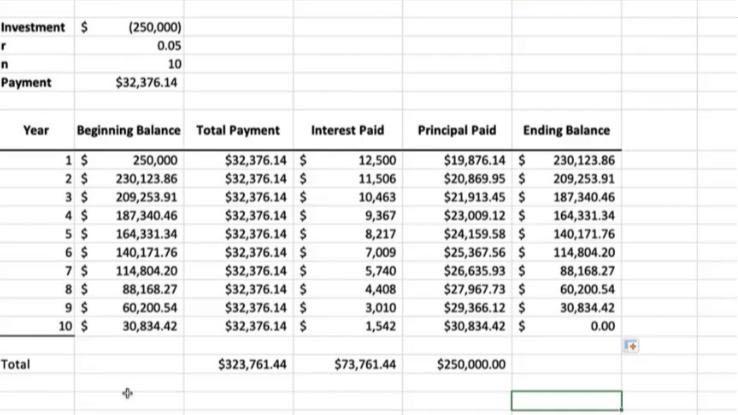

What Is an Amortized Loan?

An amortized loan is a type of loan with scheduled payments that go toward paying off both the loan'south primary corporeality and involvement. Most types of loans that you pay dorsum on a monthly ground tend to exist amortized loans — remember automobile, home equity, and personal loans. Some other great case of this type of loan structure is a fixed-charge per unit mortgage.

When you lot make monthly payments on an amortized loan, function of your payment goes to paying off interest, while the rest goes towards paying off your principal. An acquittal table is a handy fashion to summate how much of your monthly payment is going to each category, particularly since this ratio volition modify as your total residue decreases.

The average amortization table calculates several things, including:

- Monthly Balance: This column keeps a record of your total remaining residuum.

- Monthly Payment: If you have a stock-still-rate loan, this column will likely include the same payment amount each month. Once you make your payment, you lot'll exist able to subtract it from the monthly balance.

- Interest Paid: This is where you'll see how much of your monthly payment is going toward the involvement. In order to find this effigy, multiply your remaining loan balance past your monthly interest charge per unit.

- Principle Paid: Once you effigy out how much of your payment went toward paying off interest, subtract that number from the entire payment you lot made. The remaining money will exist the amount that went toward your principal.

- Remaining Balance: This is the new monthly residuum you'll start with for the next month'south payment. In other words, decrease your payment from the former monthly balance to observe the new remaining residue.

When y'all first start making payments, you'll notice that your involvement costs are at their highest. As you make more payments, however, there will be less and less primary to charge interest on. In plow, you'll notice that a picayune more of your payment will go toward paying off your principal.

How Do You Make a Loan Amortization Table?

Making your own acquittal nautical chart using Microsoft Excel, or even using an Excel loan payment template, can exist a great, firsthand way to see how information technology all works. There's even a free website called acquittal-calc.com that's able to practice the math for yous, so long equally you input your loan type, amount, interest rate, and term.

In addition to helping yous look ahead to future payments, an amortization chart tin come in handy before you even accept out a loan. For instance, while it may initially seem similar making the lowest possible payment every month is the style to get, a loan acquittal reckoner may tell a different story. That is, in some cases, by paying less each month — or selecting a longer repayment term — you may cease up paying far more than interest in the long run.

So, before settling on repayment terms, attempt running a couple of options through an amortization table to encounter what volition yield the best charge per unit overall. This strategy tin also help you decide whether refinancing a loan or, if possible, paying information technology off early is the way to go.

Loans That Do and Don't Work With an Amortization Chart

Equally helpful as an acquittal loan chart tin can be, it tin can non be used in conjunction with every blazon of loan. That is, these tables only work when forecasting installment loans or fixed-rate loans that allow yous to pay down the balance over time.

Loans that will non fit into an amortization table include the following:

Interest-Just Loans: Most mortgages are amortized loans, but others work in different ways. Involvement-only loans, for instance, only crave you to pay the involvement on the loan for a certain amount of time. This is smashing during the initial period when just the interest is due, as information technology results in much lower payments. What yous take to keep in listen, notwithstanding, is that you're not paying off your principal at all during that time. Eventually, the involvement-only period will come to an end and yous'll be expected to either pay off the loan completely or commencement making much higher payments that cover both the principal and interest.

Balloon Loans: Balloon loans are similar to involvement-but loans in that they're fun while they concluding. This is the kind of loan yous'll only want to take out if yous're expecting a huge payment at some point in the futurity. The monthly payments for airship loans start out pretty minor, but so, at some point, you'll be expected to either pay off the loan completely in a lump sum or refinance it, which isn't e'er a stable pick. For example, many people lost their homes in the mortgage crisis of 2008 by counting on the refinancing pick.

Revolving Debt: Revolving debt is the blazon you lot go into when yous use credit cards. Considering you become to choose how much you borrow and pay back each month, the main isn't always likely to stay the same, even if the involvement rate does. The only time you'd be able to use an amortization table to pay off this blazon of debt would exist if you decided to no longer use the credit card anymore and dedicated yourself to just paying it off. Even then, all the same, information technology would only work if your interest rate never changed.

Source: https://www.reference.com/business-finance/loan-amortization-table?utm_content=params%3Ao%3D740005%26ad%3DdirN%26qo%3DserpIndex

0 Response to "5-2 Review and Reinforcement Reading the Periodic Table"

Post a Comment